Reducing Equity Exposure Amid Rising Global Risks - 03/31/2026

Portfolio Adjustments

-

Diversified Portfolios

Current Stock Exposure: 87%

Benchmark Stock Exposure: 85%

Sell: -5% VEA: Vanguard FTSE Developed Markets ETF.

Buy: +5% CMNIX: Calamos Market Neutral Income Fund.

CarbonLITE Portfolios

Current Stock Exposure: 87%

Benchmark Stock Exposure: 85%

Sell:-5% EFAX: State Street SPDR MSCI EAFE Fossil Fuel Reserves Free ETF.

Buy: 5% CMNIX: Calamos Market Neutral Income Fund

ETF-Only Portfolios

Current Stock Exposure: 87%

Benchmark Stock Exposure: 85%

Sell: -5% VEA: Vanguard FTSE Developed Markets ETF.

Buy: 5% MNA: NYLI Merger Arbitrage ETF.

-

Diversified Portfolios

Current Stock Exposure: 56.5%

Benchmark Stock Exposure: 60%

Sell: -3% VEA: Vanguard FTSE Developed Markets ETF.

Sell: -2% DFAI: Dimensional International Core Equity Market ETF

Buy: +5% CMNIX: Calamos Market Neutral Income Fund.

CarbonLITE Portfolios

Current Stock Exposure: 56.5%

Benchmark Stock Exposure: 60%

Sell: -5% GCIFX: Green Century MSCI International Index Fund

Buy: +5% CMNIX: Calamos Market Neutral Income Fund

ETF-Only Portfolios

Current Stock Exposure: 56.5%

Benchmark Stock Exposure: 60%

Sell: -3% VEA: Vanguard FTSE Developed Markets ETF

Sell: -2% DFAI: Dimensional International Core Equity Market ETF.

Buy: +5% MNA: NYLI Merger Arbitrage ETF

-

Diversified Portfolios

Current Stock Exposure: 29%

Benchmark Stock Exposure: 30%

No Trades.

CarbonLITE Portfolios

Current Stock Exposure: 29%

Benchmark Stock Exposure: 30%

No Trades.

ETF-Only Portfolios

Current Stock Exposure: 29%

Benchmark Stock Exposure: 30%

No Trades.

We wanted to share a brief update on a recent portfolio adjustment and the rationale behind it.

As part of our ongoing effort to keep your portfolio aligned with the data, we have reduced our International Equity exposure and added the more defensive Calamos Market Neutral Income Fund to your portfolio.

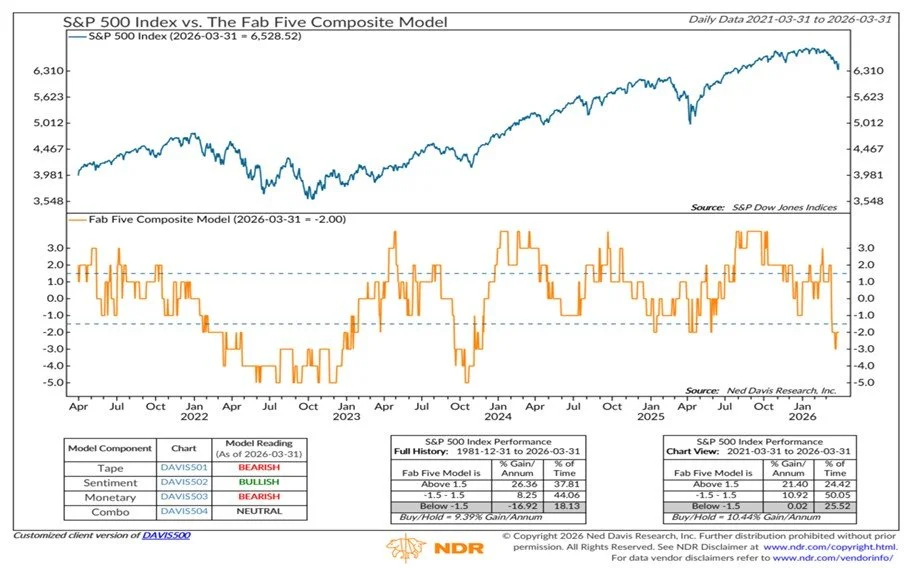

Stonehearth’s Internal risk model and the Fab Five Model from our partners at Ned Davis which can be seen below, are both indicating a meaningful deterioration in the global risk environment. Two developments have been driving the majority of this shift.

1. Rising Bond Yields Are Creating Headwinds for Risk Assets

Bond yields have risen meaningfully in recent weeks, and this move has had an increasingly negative impact on both stock and bond performance. Higher yields tend to pressure equity valuations and reduce the appeal of the fixed income asset class.

Historically, this type of environment has been more favorable to the market neutral asset class, which is less sensitive to interest‑rate volatility and provides some downside protection in times of stress.

2. Market Participation Has Weakened

We are also seeing a decline in global market participation. A growing share of stocks around the world are now trading below their long‑term trendlines. When fewer stocks remain in sustained uptrends, market advances become more fragile and the probability of pullbacks increases.

We will continue to monitor the data closely and adjust positioning as needed. Our focus remains on protecting your long‑term financial goals while navigating the current environment with discipline and care.

You’ll receive a trade confirmation from Charles Schwab reflecting these transactions. If you'd like to walk through these trades or discuss the positioning in more detail, we are happy to schedule a time to talk.

We're here to help you stay grounded, informed, and positioned for the long term, even when the market isn’t making it easy.

Warm regards,

SCM Investment Committee